There is a distinction that rarely surfaces in discussions about corporate gift type selection, but which explains a significant proportion of the cases where a well-funded gifting programme produces gifts that recipients do not use. The gift type that gets selected is not always the gift type that would best serve the recipient. It is, more often, the gift type that most efficiently clears the internal approval process. These two outcomes are not the same, and the gap between them is where most corporate gifting programmes quietly fail.

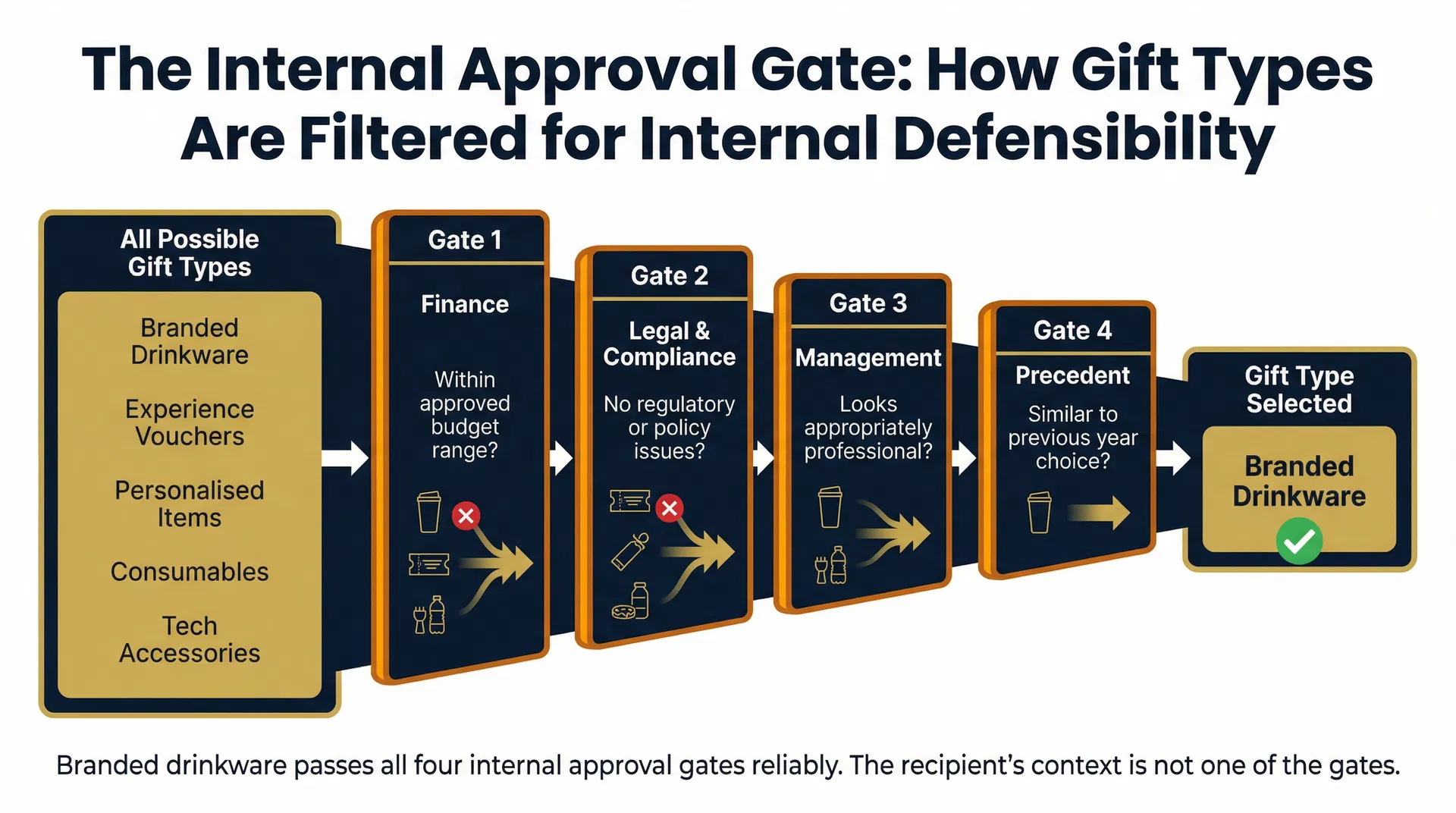

In any organisation with a structured procurement function, a gift type decision passes through multiple internal stakeholders before it reaches a supplier. Finance evaluates whether the unit cost falls within the approved budget range. Legal or compliance reviews whether the gift type creates any regulatory exposure or violates the organisation's gifting policy. Management assesses whether the gift looks appropriately professional and consistent with the organisation's brand positioning. And implicitly, everyone involved in the decision checks whether the gift type is consistent with what was sent in previous cycles — because a choice that departs significantly from precedent requires justification, and justification requires effort. The gift type that clears all four of these gates most efficiently is the one that gets selected.

Branded drinkware — insulated bottles, tumblers, travel mugs — passes all four gates with minimal friction. The unit cost is predictable and available across a wide range of price points, making it easy to match to any approved budget. It carries no meaningful compliance risk: it is not alcohol, not food with allergen implications, not a luxury item that triggers anti-bribery thresholds in most jurisdictions. It photographs well and reads as professionally appropriate in any management review. And it has been selected by enough organisations over enough years that it is the closest thing to a precedented default in the corporate gifting category. The result is that branded drinkware wins the internal approval process reliably — not because it is the best gift type for the recipient, but because it is the most defensible gift type for the people making the decision.

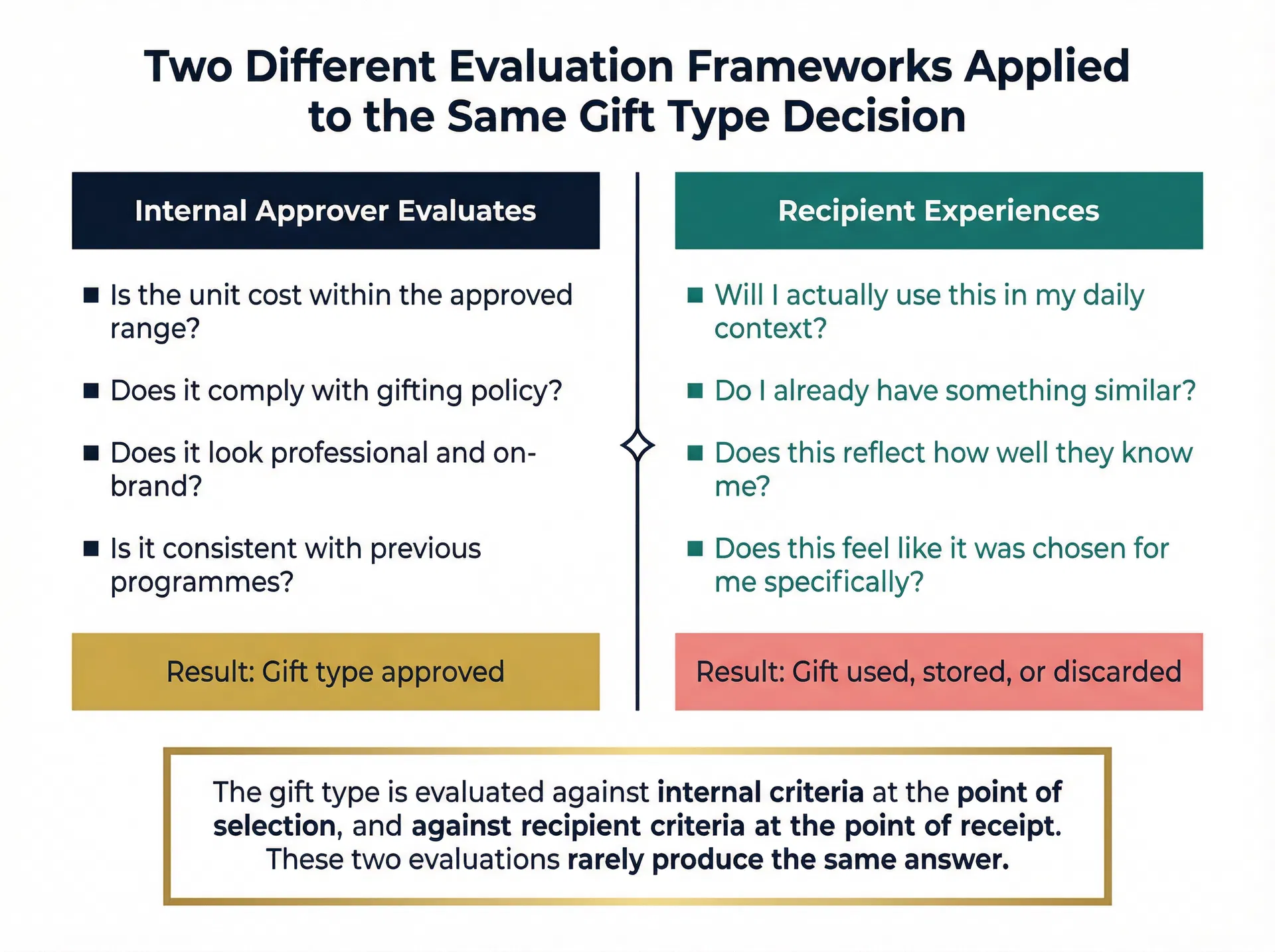

The problem with optimising for internal defensibility is that the internal approval process evaluates the gift type against criteria that have nothing to do with how the recipient will experience it. Finance asks whether the cost is within range; the recipient asks whether they will actually use the item in their daily context. Legal asks whether the gift creates compliance exposure; the recipient asks whether they already have three similar items on their desk. Management asks whether the gift looks on-brand; the recipient asks whether it feels like it was chosen with any knowledge of who they are. These are two entirely different evaluation frameworks applied to the same decision, and they rarely produce the same answer.

In practice, this is where gift type decisions start to be misjudged most systematically — not in any single programme, but across the entire category of organisations that run structured gifting programmes. The internal approval process is a legitimate and necessary part of procurement governance. The issue is not that it exists, but that it has become the primary filter for gift type selection, displacing the question of recipient value entirely. When a procurement team can point to a gift type that is within budget, compliant, professionally appropriate, and consistent with precedent, the discussion about whether the recipient will actually value it tends not to happen. The internal case has already been made.

This dynamic is particularly consequential for organisations where the gifting programme is intended to serve a relationship function — to signal investment in a specific client relationship, to acknowledge a partnership milestone, or to differentiate the organisation's approach to key accounts. A gift type selected for internal defensibility cannot serve these functions, because internal defensibility is a property of the gift type's relationship to the organisation's own processes, not to the recipient's context. A premium branded insulated bottle is internally defensible. Whether it communicates anything meaningful to the specific recipient who receives it depends entirely on factors — their daily habits, their existing collection of branded items, their sense of whether the gift was chosen with them in mind — that the internal approval process has no mechanism for evaluating.

The broader question of how to align gift type selection with recipient context, rather than internal approval criteria, is one that systematic approaches to corporate gift type decisions address by restructuring the evaluation sequence rather than bypassing the approval process. The approval gates are not the problem. The problem is that they are currently the only gates — and recipient context is not among them.

The reason this pattern is so persistent is structural. The internal approval process is visible, auditable, and produces a clear outcome: approved or not approved. The question of whether the recipient will value the gift is invisible at the point of selection, and its answer only becomes apparent weeks or months later when the gifting programme's relationship impact — or lack of it — becomes observable. By that point, the gift type decision has long since been made, the order has been placed, and the next cycle is already beginning with the same precedent in place. The internal approval optimisation problem reproduces itself precisely because its consequences are deferred and diffuse, while its causes are immediate and institutionally reinforced.